The current discussion around digital money is often too technical.

In reality, it is about something much more fundamental:

![]() The question of the monetary anchor in a digital world

The question of the monetary anchor in a digital world

The ECB has taken a very clear position:

The Euro is intended to serve as an anchor to preserve trust in private money.

Two principles are at the core:

- Singleness of Currency

→ All forms of money must be convertible 1:1 at all times - Hierarchy of Money

→ Central bank money is the safest form

→ Bank deposits and private money are merely claims on it

This is economically sound thinking.

However, it creates a structural tension:

![]() The more attractive the digital euro becomes, the greater the risk of disintermediation

The more attractive the digital euro becomes, the greater the risk of disintermediation

→ Deposits move away from commercial banks

→ Banks’ ability to lend is reduced

This is why the ECB operates within the so-called “options triangle”:

- Ensuring stability

- Protecting banks

- Enabling innovation

![]() It is impossible to maximize all three at the same time.

It is impossible to maximize all three at the same time.

In parallel, a very different approach is emerging in the United States:

- Stablecoins are actively promoted and, in part, framed as currency competition

- Backed by government bonds and cash

- Positioned as a tool to strengthen global USD dominance

However, dollar-based stablecoins do not represent true competition according to Hayek,

as they rely on the same underlying anchor—similar to the euro concept.

The result:

![]() Europe and the U.S. are currently providing two very different answers to the same question – and both are incomplete.

Europe and the U.S. are currently providing two very different answers to the same question – and both are incomplete.

Both approaches overlook a critical driver:

![]() The emergence of money within real-economy ecosystems:

The emergence of money within real-economy ecosystems:

- Money is increasingly created within platforms and ecosystems

- Companies are taking over more payment and loyalty functions

- Customers no longer operate solely within the banking system

The tension we are seeing today is not new.

A look at history reveals two recurring patterns:

- Prussia (1750–1755)

Frederick the Great attempted to establish a unified currency standard with the “Reichstaler”.

![]() Result: failed on Reich‘s level

Result: failed on Reich‘s level

Why?

Without broad political support, no functioning monetary anchor can emerge.

Acceptance only emerges when a currency works in everyday life.

- England in the 19th century

Two schools of thought clashed:

- Currency School

→ hard backing, strict rules, maximum stability - Banking School

→ flexible money supply, adaptation to economic activity

![]() Both were right.

Both were right.![]() Both were not viable on their own.

Both were not viable on their own.

The key insight from this – also clearly highlighted in the current IBF paper by Prof. Dr. Jan Greitens:

![]() A functioning monetary system always requires:

A functioning monetary system always requires:

a stable anchor + sufficient elasticity for the economy (trade, investment and growth)

This is exactly where current approaches driven by digitaliztion of money fall short:

- Europe: The digital euro prioritizes stability

- U.S.: Stablecoins prioritize flexibility

- Both risk structural weaknesses

At the same time, something new is emerging:

![]() Companies are beginning to think in terms of their own currencies

Companies are beginning to think in terms of their own currencies

→ for customer loyalty

→ for payments

→ for ecosystems

This leads to a new question:

![]() How do you prevent fragmentation without stifling innovation, e.g. in corporate currencies?

How do you prevent fragmentation without stifling innovation, e.g. in corporate currencies?

When companies introduce their own currencies, a new system emerges:

- Each major brand optimizes its currency for its own ecosystem

- Money becomes purpose-bound and usage-driven

- The money supply can grow elastically

![]() This closely follows the logic of the Banking School

This closely follows the logic of the Banking School

But it also creates a risk:

![]() Fragmentation

Fragmentation

This is exactly where Leondrino comes in:

![]() A structured framework instead of an uncontrolled stablecoin landscape

A structured framework instead of an uncontrolled stablecoin landscape

Core elements:

- Limited issuance in early phases

- Acceptance obligations for products and services

- Fractional reserve structures in higher quality stages

However, the key building block is:

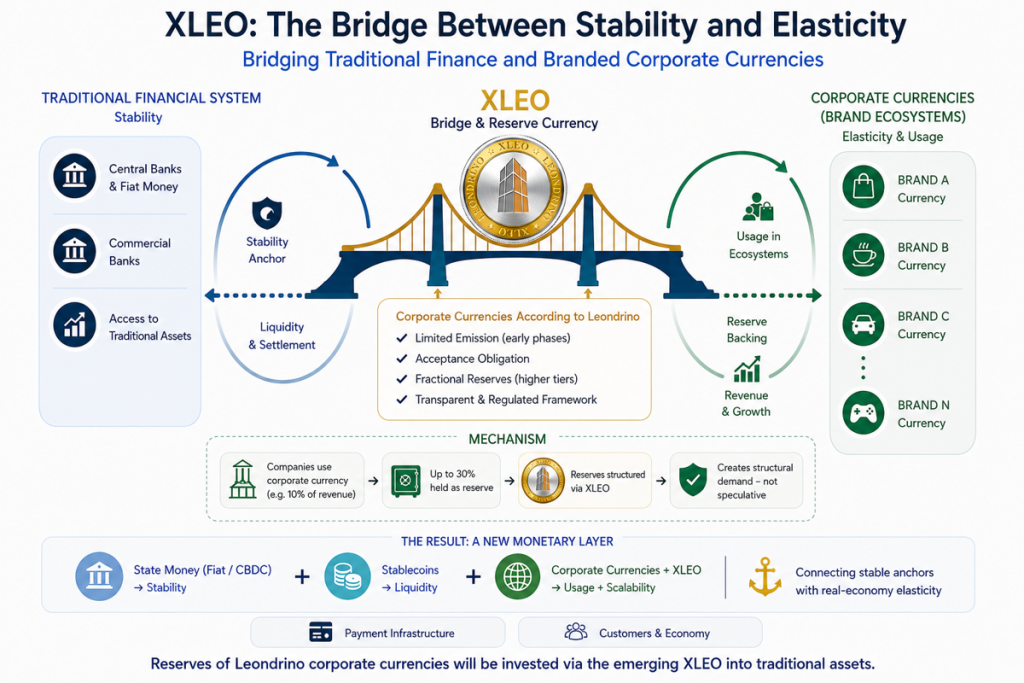

![]() XLEO as a bridge and reserve currency

XLEO as a bridge and reserve currency

The mechanics are critical:

- Companies use their corporate currency for a portion of their revenue

(e.g. 10% as an initial scenario) - of which up to 30% is held as reserve

- this reserve is, over time, structured via XLEO

This creates something fundamentally new:

![]() Structural demand — not speculative demand

Structural demand — not speculative demand

Thought experiment (7–10 years):

10 global companies

Ø revenue: USD 100 billion

→ 10% via corporate currency = USD 10 billion

→ 30% reserve = USD 3 billion per company

![]() Result:

Result:

USD 30 billion potential reserve demand

Facing an initial limit of 1 billion XLEO during its initial rollout phase.

![]() To meet the demand based on the planned future role of XLEO, a transition is planned:

To meet the demand based on the planned future role of XLEO, a transition is planned:

From the fixed limit of 1 billion XLEO to dynamic supply management

supervised by a Monetary Board

(with the later migration to Leondrino token class A)

(Currently, XLEO is still in token class C and limited to a utility role in the Leondrino ecosystem.)

Now the key point:

![]() This demand is driven by

This demand is driven by

- customer relationships

- real revenues

- functioning business models

not by trading.

What does this mean for the monetary system?

We expect the emergence of an additional new layer:

- State money (Fiat / CBDC) → Stability

- Stablecoins → Liquidity

Corporate currencies + XLEO → Usage in real economy + scalability

Corporate currencies + XLEO → Usage in real economy + scalability

My thesis:

The future monetary system will not be dominated by a single solution.

![]() It will become modular and more competitive on the private side.

It will become modular and more competitive on the private side.

And XLEO in its future role addresses exactly the gap

that neither states nor first generation stablecoins solve properly:

![]() Connecting stable anchors with real-economy elasticity

Connecting stable anchors with real-economy elasticity

Peter Reuschel

Co-founder of Leondrino and Managing Director of Leondrino Germany